The Erosion of Trust

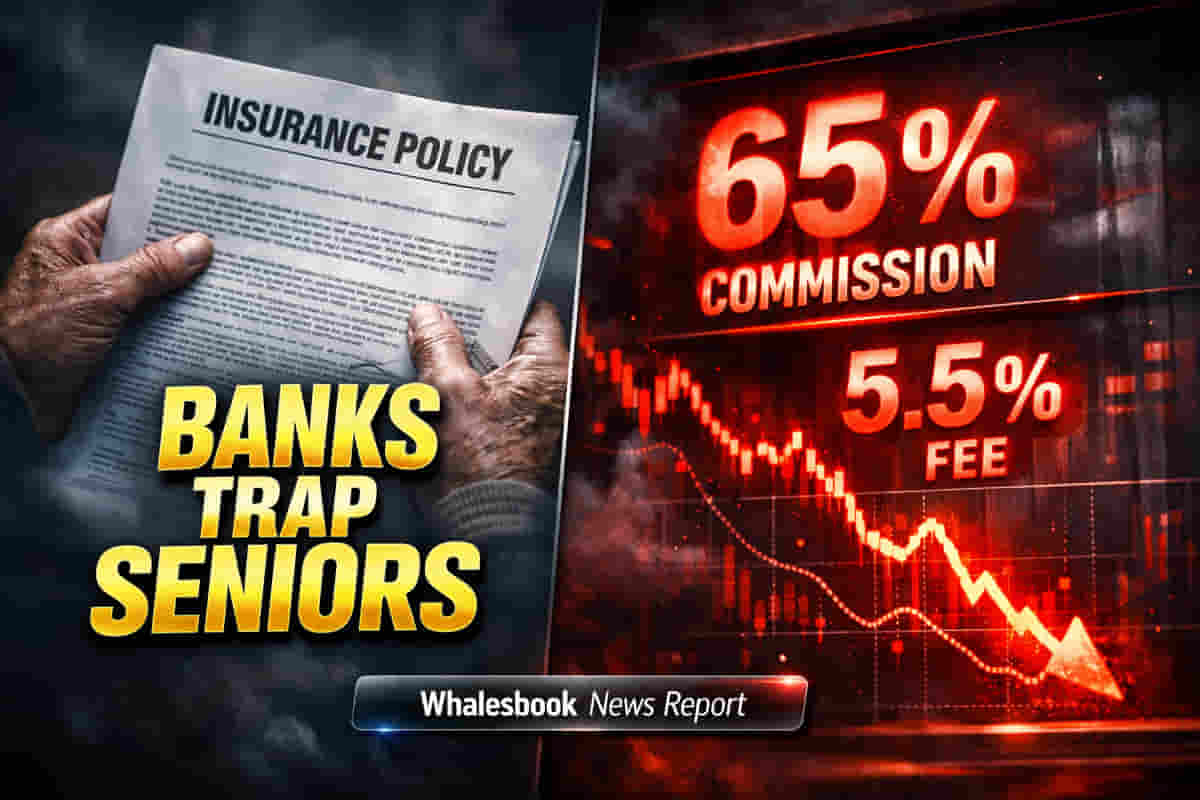

Banks in India are increasingly exploiting the trust of senior citizens, pushing unsuitable, high-commission insurance products instead of traditional savings schemes. This practice targets retirees who frequently visit branches for routine transactions, turning everyday interactions into sales opportunities. The outcome is significant financial losses for the elderly and a surge in regulatory complaints, highlighting a systemic issue.

Incentive-Driven Sales

The core driver is incentive-based selling. Financial intermediaries, including bank staff, earn substantial commissions on insurance products, often far exceeding those for mutual funds. Distributors can earn between two and eleven times more in first-year commissions. This lucrative structure encourages the mis-selling of policies as 'FD-like' or 'guaranteed' to trusting seniors, despite long lock-in periods and low effective returns, sometimes as low as 4-6% compared to government-backed schemes.

Rising Grievances

Regulatory data confirms a sharp increase in such practices. Complaints classified as 'Unfair Business Practices' rose by approximately 14% to 26,667 in FY25, now accounting for over 22% of all grievances against life insurers. In FY24, the top 15 listed banks collectively earned around ₹21,773 crore in commission income from distributing third-party products, with commission income exceeding a quarter of total income for some institutions.

Proposed Safeguards

Experts argue that existing safeguards are often mere procedural checkboxes. They propose classifying sales to senior citizens as high-risk, triggering mandatory financial underwriting. Additional measures suggested include separate recorded consent calls for family members named as life insured and automatically flagging sales of long-term policies to the elderly where returns begin at advanced ages. Stronger accountability through public disclosure and genuinely punitive penalties is deemed essential.